Australia's mandatory climate reporting framework is now in effect. ASRS S2 - formally the Australian Sustainability Reporting Standard S2 Climate-related Financial Disclosures - applies to thousands of Australian entities across three compliance groups, with the first Group 1 reports due for financial years beginning on or after 1 January 2025.

This guide covers everything you need to know: who must comply, what the standard actually requires, how the timelines work, and what you need to do now. Use the navigation below to go directly to the section most relevant to your situation.

Primary sources: AASB ASRS standards | ASIC mandatory climate reporting guidance | Treasury mandatory climate reporting

This guide is written for three audiences. Jump to the section most relevant to you.

CFOs and Finance Directors

You need to understand scope, cost, assurance obligations, and what goes in the financial report. Jump to: Which Australian companies are required to comply?

Sustainability Managers and Reporting Leads

You need to understand the four disclosure pillars, Scope 3 requirements, and what auditors will look for. Jump to: What does ASRS S2 require Australian companies to disclose? and How does ASRS S2 handle Scope 3 emissions?

Board Directors

You have personal governance obligations under ASRS S2 that go beyond signing off reports. Jump to: What does ASRS S2 require Australian companies to disclose? - specifically the Governance pillar - and read the full ASRS Governance Requirements guide.

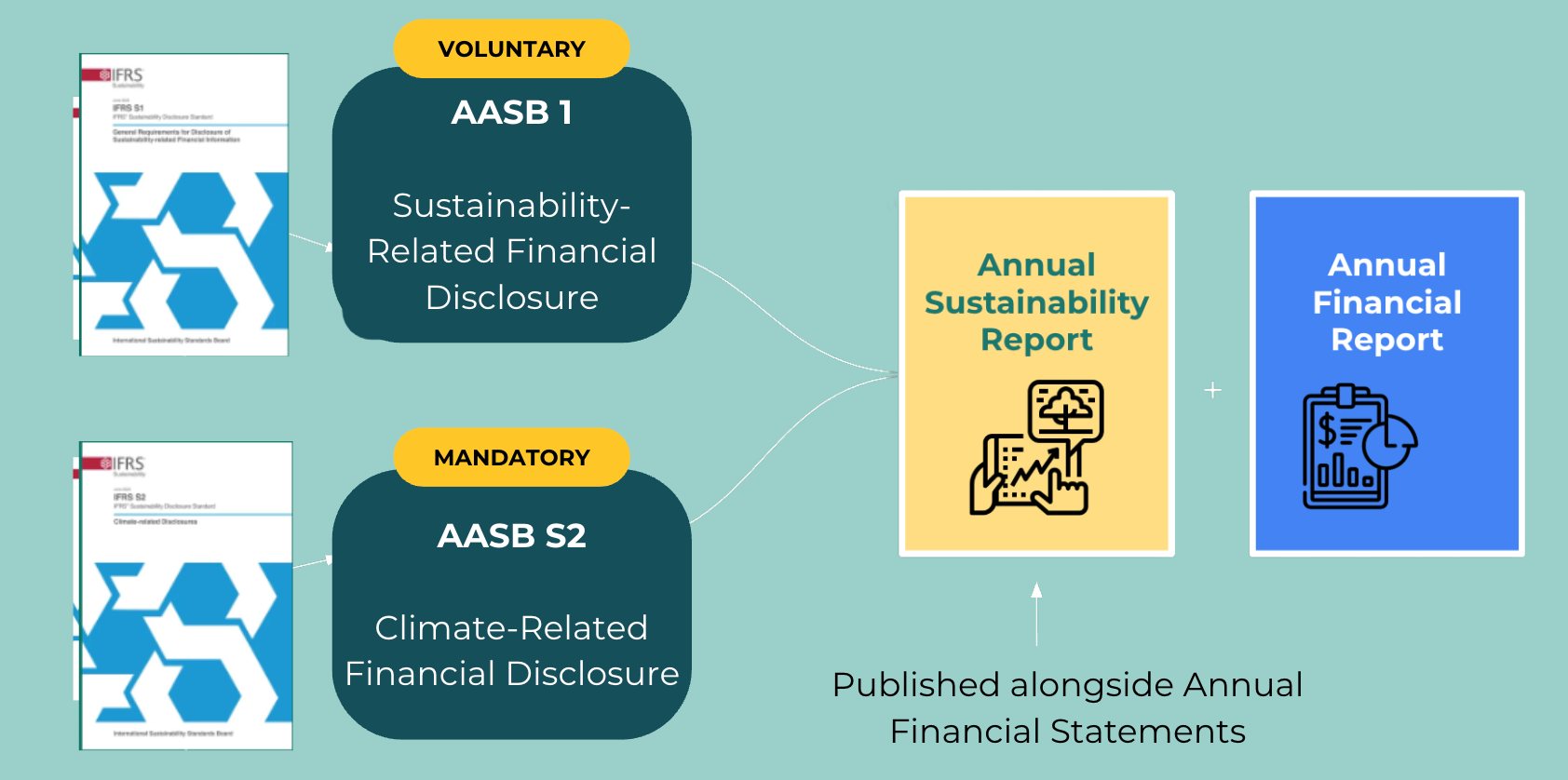

ASRS S2 was issued by the Australian Accounting Standards Board (AASB) and operates under the Corporations Act 2001, as amended by the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024. It is based on IFRS S2, the global baseline standard issued by the International Sustainability Standards Board (ISSB), with Australian-specific modifications.

Is ASRS S2 the same as AASB S2? Yes. ASRS S2 and AASB S2 refer to the same standard. "ASRS" stands for Australian Sustainability Reporting Standard. The AASB administers and issues the standard. Both names appear in the market, often used interchangeably.

ASRS S2 applies alongside ASRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information), which sets the overarching framework for how disclosures should be presented. Most reporting entities will need to comply with both.

The compliance obligation is determined by size thresholds across three criteria: consolidated revenue, consolidated gross assets, and number of employees. Entities that meet two or more of the three thresholds for their group are in scope.

Proposed change (2026-27 Federal Budget - not yet law):

The government has proposed lifting the “large proprietary company” reporting thresholds under the Corporations Act from $50m to $100m in consolidated revenue and from $25m to $50m in consolidated gross assets (the 100-employee test is unchanged). Because Group 3 eligibility is tied to these thresholds, some entities that would currently fall into Group 3 could drop out of mandatory reporting altogether. This reform is subject to consultation and had not been legislated as of July 2026. Groups 1 and 2 thresholds are unaffected. If you are near the Group 3 boundary, confirm your position before assuming you are in or out of scope.

Note: These thresholds apply to Australian entities lodging financial reports under the Corporations Act. Large proprietary companies, foreign-owned entities, and registered managed investment schemes may have different trigger points. Check the ASIC guidance on who must comply for your specific entity type.

Not sure if you're in scope?

Book a 30-minute scoping call with Trace - we can confirm your compliance group and what you need to have ready.

For most Australian entities, ASRS S1 and ASRS S2 are reported together and treated as an integrated disclosure package. The practical focus for most first-year reporters is ASRS S2, because that is where the most detailed - and most commercially sensitive - disclosures sit.

If your organisation operates across multiple jurisdictions, you may face obligations under more than one framework. Trace can help you map your obligations and identify where reporting requirements overlap.

.png)

Trace works with businesses at every stage of their mandatory reporting journey, from first emissions measurement to audit-ready ASRS S2 disclosure. Talk to our team to see how we can help.

Under ASRS S2, the board of directors must actively oversee climate-related risks and opportunities — not delegate this entirely to management. Specific requirements include:

What auditors look for: evidence that climate is a standing agenda item at board level, board minutes referencing climate risk, board skills matrix including relevant expertise, and linkage between climate performance and executive remuneration.

This is where most entities find the disclosure requirements most challenging. ASRS S2 requires you to describe:

What auditors look for: scenario analysis that is genuinely integrated into strategic planning (not a standalone exercise), financial quantification of climate risks even where estimates involve significant uncertainty, and consistency between the climate disclosures and what the financial statements say about risk.

Entities must describe their processes for identifying, assessing, managing, and monitoring climate-related risks — and explain how these processes are integrated into the overall enterprise risk management framework.

Specific disclosures include:

What auditors look for: a risk management process that treats climate with the same rigour as financial, operational or reputational risk — documented, reviewed, and integrated into board-level risk reporting.

ASRS S2 requires disclosure of:

What auditors look for: emissions data that is traceable to source, consistent methodology between years, evidence that Scope 3 estimates are based on reasonable assumptions, and targets that are specific and trackable rather than aspirational.

What needs to happen before your first report date:

Group 2 note: If your financial year runs July to June, your first mandatory ASRS S2 report covers the period starting 1 July 2026 - meaning preparation work needs to be underway now.

Scope 3 is typically the most challenging disclosure for Australian entities. For many businesses, particularly those in manufacturing, financial services, or retail, Scope 3 can represent 70–90% of total emissions. The GHG Protocol's Corporate Value Chain (Scope 3) Standard defines 15 categories of upstream and downstream emissions, from purchased goods and services through to the use and disposal of sold products.

What "material categories" means: Entities are not required to report every Scope 3 category - only those that are material to the business. However, the bar for what is material is set by the standard, not by what is convenient to measure. A financial institution's financed emissions (Category 15) will almost certainly be material. A large retailer's purchased goods and services (Category 1) will be material.

Preparing before the relief period ends:

The Scope 3 relief period is an opportunity to build your measurement capability, not to defer the problem. Entities that use the relief period to establish supplier data collection processes, identify material categories, and run initial estimates will be in a far stronger position when mandatory disclosure arrives.

See our GHG Protocol Scope 3 guide for detailed guidance on category classification and the proposed 95% coverage threshold.

ASRS S2 (Australian Sustainability Reporting Standard S2) is the mandatory climate-related financial disclosure standard issued by the Australian Accounting Standards Board. It requires in-scope entities to disclose climate governance, strategy, risk management, and emissions data. Reporting begins for Group 1 entities (the largest companies) for financial years starting on or after 1 January 2025, with Group 2 beginning from July 2026 and Group 3 from July 2027.

Yes. ASRS S2 and AASB S2 refer to the same standard. ASRS stands for Australian Sustainability Reporting Standard. The AASB (Australian Accounting Standards Board) issues and administers the standard. Both names appear in the market and are used interchangeably by companies, advisors and regulators.

Australian entities that meet two or more of three size thresholds — revenue, assets, and employees — are required to comply. The thresholds differ by compliance group. Group 1 applies to the largest entities (revenue over $500m, assets over $1bn, or more than 500 employees), Group 2 to mid-size entities, and Group 3 to smaller but still substantial entities. Certain entity types such as large proprietary companies and registered managed investment schemes also have obligations. The ASIC guidance on mandatory climate reporting sets out the full scope.

ASRS S2 requires disclosure across four pillars. Governance: how the board oversees climate-related risks and opportunities. Strategy: how climate affects the business model, financial position and planning. Risk Management: how climate risks are identified, assessed, managed and monitored. Metrics and Targets: quantitative data on emissions, climate-related financial exposures, and progress against climate targets.

ASRS S2 is the Australian version of ISSB IFRS S2, with modifications for the Australian context. The key differences are: Australia's phased approach to Scope 3 reporting (relief in early years), Australia's three-group compliance schedule, and specific ASIC guidance on presentation and lodgement. The substance of the disclosure requirements — the four pillars, the scenarios, the emissions methodology — is substantially aligned with ISSB S2.

No. Every entity gets a one-year exemption from Scope 3 disclosure in its first reporting year. From the second reporting period, Scope 3 reporting across all material GHG Protocol categories becomes mandatory - this applies equally to Groups 1, 2 and 3. The relief period is intended to give entities time to build measurement capability, not to avoid the requirement altogether.

ASRS S2 is enforced under the Corporations Act. ASIC has indicated it will take a graduated enforcement approach in early years, focusing on engagement and guidance rather than immediate penalties. However, failure to include required climate disclosures in an annual report is a breach of the Act. Directors can be personally liable for misleading or incomplete disclosures, including those relating to climate risk. Assurance requirements also mean that omissions are likely to be identified in the audit process.

For a mid-size Group 2 entity starting from a low base, realistic preparation time is 12–18 months before the first report is due. The critical path is usually data: establishing Scope 1 and 2 measurement, completing a climate risk assessment, and running scenario analysis. Entities that already have sustainability reporting infrastructure can often compress this to 6–9 months. Trace's ASRS Readiness Guide outlines the seven steps in detail.

Directors are required to demonstrate active oversight of climate-related risks and opportunities — not just sign off on a document produced by management. This includes: understanding the climate-related risks material to the business, overseeing the climate risk management framework, monitoring progress against any climate targets, and ensuring the accuracy of disclosures included in or with the annual report. Some boards are amending their charters and skills matrices to formalise this. The ASRS Governance guide covers each requirement in detail.

You do not legally require specialist software, but most entities find that trying to manage ASRS compliance in spreadsheets creates audit risk and significant manual effort. The main functions software provides are: emissions calculation and data management, scenario analysis outputs, disclosure drafting, audit trails for assurance, and year-on-year comparatives. Trace is built specifically for ASRS and ISSB compliance, with modules that match the compliance stage of each group — so you're not paying for capabilities you don't yet need.

Manual spreadsheet approaches carry significant audit risk: formula errors, inconsistent methodology, and missing audit trails are the most common sources of assurance findings. Read more: Common errors hiding in spreadsheet-built carbon inventories

Ready to understand your ASRS obligations?

Trace is a climate reporting platform specialising in ISSB and AASB standards. We work with Australian entities across Group 1, 2 and 3 to build disclosure-ready reporting programmes, without the Big 4 price tag.

London - Sydney

.png)

.webp)