What's the biggest challenge Australian businesses face with ASRS compliance?

Spoiler: It's the third option.

Australian businesses interviewed by Trace are already deep into preparing for ASRS compliance, and their feedback might surprise you. The real challenge isn't mastering technical requirements or managing costs, it's cutting through the confusion about what actually needs to be done, when, and how much it should realistically cost.

Since 1 January 2025, the Australian Sustainability Reporting Standards (ASRS) have required eligible companies to disclose climate-related financial information alongside their annual statements. This isn't just another compliance box to tick, it's fundamentally reshaping corporate transparency in Australia.

What makes this guide different?

No regulatory jargon. No theoretical frameworks. Just real insights from companies navigating ASRS compliance right now. Their candid experiences reveal six critical themes every business needs to understand before diving in.

Who is this for?

Download The ASRS Pulse Report

The Australian Sustainability Reporting Standards represent Australia's commitment to mandatory climate-related financial disclosures, aligning with international frameworks like the Task Force on Climate-related Financial Disclosures (TCFD) and International Financial Reporting Standards (IFRS).

ASRS applies to:

The implementation follows a phased approach:

AASB S1: General Requirements for Disclosure of Sustainability-related Financial Information

This standard sets the foundation for sustainability reporting, covering governance, strategy, risk management, and metrics.

AASB S2: Climate-related Disclosures

This standard specifically addresses climate-related risks and opportunities, including emissions reporting across all three scopes.

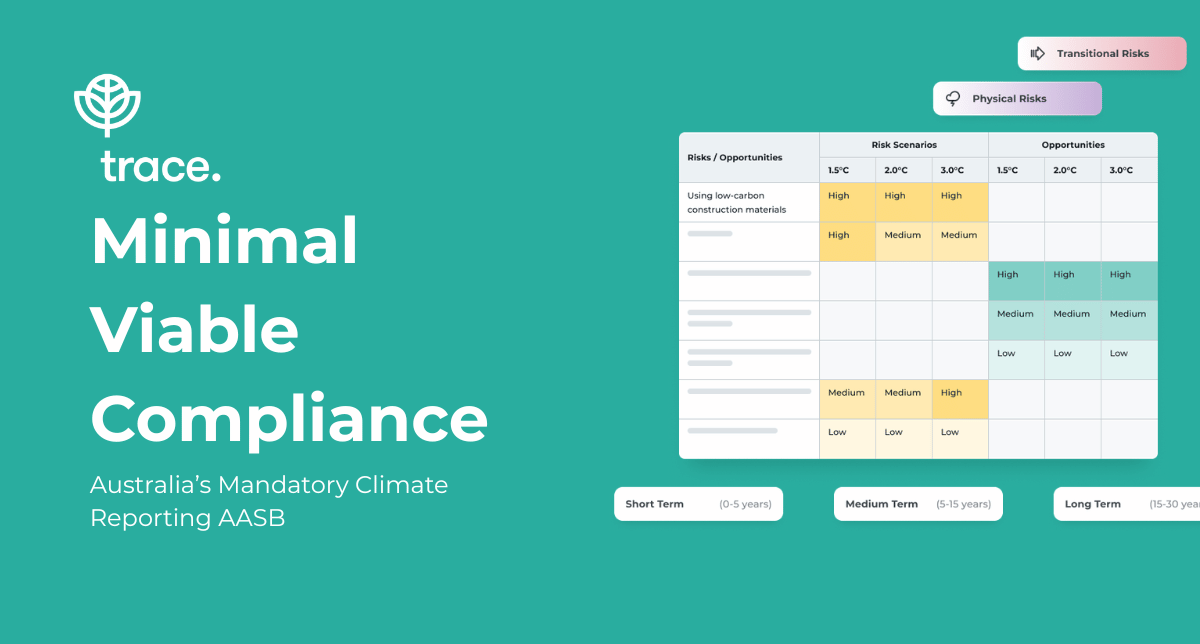

The standards aren't just about compliance. They're reshaping how businesses think about climate risk and opportunity. Companies report that ASRS preparation is driving conversations about:

Our research with over 20 companies preparing for ASRS revealed six consistent themes that cut across industries, from retail and manufacturing to legal services and logistics.

One of the most surprising findings was how external pressure is proving as influential as the regulation itself. Companies consistently report that client and investor expectations are pushing them to act on climate disclosures just as much as legal requirements.

"Client and investor expectations are as strong a driver as regulation," explained one retail sector executive. This pressure manifests in three key ways:

Supply Chain Mandates

Organisations across industries are "feeling the heat from B2B clients" who require carbon disclosures from suppliers. This customer-driven compliance means even companies not yet legally obliged are starting ASRS preparations to meet client contracts.

A sustainability manager described how a major customer wrote climate targets directly into their contract, essentially telling them "do that [report your carbon footprint] or don't do business with us."

Investor Expectations

Investors are asking pointed questions about climate readiness, effectively making ASRS-related transparency part of due diligence. This adds urgency, especially for companies seeking investment or facing ESG-minded shareholders.

Peer Pressure Across Sectors

Interviewees noted that no industry feels insulated. From retail to professional services, there's a pervasive sense that "if we don't start reporting, we'll fall behind our peers." Many are acting now to preserve reputation and market position.

Nearly every company expressed confidence in handling Scope 1 and 2 emissions (direct operational emissions and purchased energy), but Scope 3 emissions tell a different story entirely.

The complexity of accounting for value-chain impacts - from suppliers to product use - is creating widespread confusion and data gaps. A CFO from an engineering firm captured the universal sentiment: "Scope 1 and 2 are relatively easy for us - Scope 3 is where it gets really messy."

Why Scope 3 Is Different

The good news is that ASRS provides a one-year relief period for Scope 3 reporting, making it mandatory from the second reporting period. This gives companies time to build systems and relationships with suppliers.

Practical Impact

Companies are seeking guidance on what constitutes a "good" Scope 3 target and how to confidently link their data to long-term emissions goals. As one sustainability lead put it: "We can handle our emissions… but we need help bridging the gap to metrics and targets."

While sustainability teams dive deep into data collection and analysis, many boards and C-suites are only beginning to grasp what ASRS actually entails for their oversight responsibilities.

A COO at an advertising company admitted: "Our auditors aren't ready yet - and neither is our board." This sentiment echoes across sectors, highlighting three critical gaps:

Board Knowledge Deficits

Many directors have minimal experience with TCFD or sustainability reporting frameworks. Companies report an urgent need for board training on climate risk and governance to ensure directors can fulfil their oversight role under ASRS.

Auditor Uncertainty

Even external auditors are still figuring out the new standards. Companies report that guidance on what auditors will expect - especially regarding limited versus reasonable assurance in early years - is still evolving. This creates anxiety for finance teams who don't want surprises when audits begin.

Documentation and Controls

A common question is how to document climate-related governance and controls to satisfy audit standards. Many firms lack formal processes like board-reviewed climate strategies and documented risk assessments, and are now rushing to create them.

Despite the challenges, there's a remarkable theme of optimism among companies with strong existing ESG cultures. These organisations are determined to use ASRS as a catalyst for broader strategy rather than treating it as a compliance checkbox.

"This isn't just about ticking a box - we're using it to formalise our values," said one sustainability lead at a retail company. This strategic mindset manifests in several ways:

Values Into Action

Companies with established sustainability values are reframing ASRS as a framework to formalise and showcase what they already care about. Instead of a mere compliance task, reporting becomes a project of codifying values into formal climate policies and publicly stated targets.

Competitive Differentiation

Several participants noted that early compliance could differentiate them in the market. Being able to provide audited emissions data is becoming an advantage in procurement, as clients and government tenders increasingly favour bidders with credible climate credentials.

Enhanced Investor Relations

Transparent reporting is viewed as a way to strengthen investor relations by demonstrating long-term risk management capabilities and strategic thinking about future challenges.

Cultural Alignment

Rather than resisting the new rules, these organisations are telling staff that ASRS aligns with company mission. By "formalising our values," they signal that climate accountability is now part of business as usual, helping rally internal support.

Perhaps the most universal request from businesses is for clear, phased roadmaps that break down the path to full ASRS compliance into manageable chunks.

"What does 'good' look like between now and 2027?" asked one law firm partner, capturing a widespread plea for guidance. The lack of clarity on interim milestones - especially given the staged implementation - leaves businesses unsure how to pace themselves.

What companies are requesting:

Phased Timelines

Organisations want concrete timelines detailing what should be accomplished in the next 6, 12, and 18 months. Common requests include clarity on when to have emissions baselines completed, governance structures defined, and draft reports prepared.

Practice Runs and Pilots

Many businesses plan to conduct internal "dry runs" of reporting before it's legally required. This might involve producing a dummy sustainability report or undergoing informal audits of climate data in advance. One interviewee noted their "practice run" in FY23 "made all the difference" in being prepared.

Templates and Benchmarks

There's high demand for templates, checklists, and examples to demystify ASRS requirements. Companies want sample disclosure frameworks, lists of required metrics, and writing examples to ensure their reports hit the mark.

One of the most frustrating aspects of ASRS preparation has been the wild variation in quotes from external providers. Companies report receiving proposals ranging from low five-figure sums to over $200,000, creating widespread confusion about appropriate budgeting.

"We've seen quotes north of $200,000 for full ASRS support - it's eye-watering," said one executive. Another finance manager voiced typical frustration: "We just want to make sure we're not duplicating work from last year. The more detail in the quote, the better."

Why Costs Vary So Dramatically

Bundled vs. Modular Services

Part of the confusion stems from what's included in each quote. Some consultants offer end-to-end packages bundling carbon footprinting, climate risk assessment workshops, audit preparation, and report writing. Others price each element separately, making apples-to-apples comparisons difficult.

Market Immaturity

The huge range suggests an immature market where providers themselves differ on the effort required or technology solutions available. This creates uncertainty for businesses trying to evaluate fair value.

Scope Variations

Companies are keen not to pay for work they've already completed elsewhere. If they have recent emissions inventories or climate risk registers, they don't want consultants redoing work from scratch.

What Businesses Want

.png)

Trace works with businesses at every stage of their mandatory reporting journey, from first emissions measurement to audit-ready ASRS S2 disclosure. Talk to our team to see how we can help.

Based on insights from companies already in progress, here's a practical 24-month roadmap for ASRS preparation:

6 Month Checkpoint:

12 Month Checkpoint:

18 Month Checkpoint:

Rather than generic "help with ASRS," companies are requesting specific support across five categories:

ASRS compliance represents both a challenge and an opportunity for Australian businesses. The companies already on this journey share common struggles: Scope 3 confusion, board education needs, cost uncertainty, and roadmap clarity, but they also demonstrate that early action and strategic thinking can turn regulatory compliance into competitive advantage.

The key lessons from businesses already in progress are clear:

Your immediate next steps should focus on assessment and planning:

Remember: ASRS compliance isn't just about meeting regulatory requirements. Done thoughtfully, it can strengthen client relationships, enhance investor confidence, improve risk management, and position your organisation as a leader in the transition to a sustainable economy.

The businesses already on this path are proving that with the right approach, ASRS compliance can be transformative rather than burdensome. The question isn't whether you'll need to comply, it's whether you'll use this requirement to build a stronger, more resilient business.

What is ASRS and when does it start?

ASRS (Australian Sustainability Reporting Standards) became mandatory on 1 January 2025, requiring eligible companies to disclose climate-related financial information alongside annual financial statements. The standards include AASB S1 (general sustainability requirements) and AASB S2 (climate-specific disclosures).

Who needs to comply with ASRS requirements?

ASRS applies to companies required to lodge audited annual financial statements under the Corporations Act 2001, including large proprietary companies and public companies meeting specific thresholds, as well as entities voluntarily preparing general purpose financial statements.

What's the difference between Scope 1, 2, and 3 emissions?

How much does ASRS compliance typically cost?

Costs vary dramatically, from tens of thousands to over $200,000, depending on company size, current capabilities, risk appetite and chosen approach. The variation reflects bundled vs. modular services, existing sustainability work, and internal vs. external resource allocation.

Can we do ASRS compliance in-house or do we need consultants?

Many companies successfully use hybrid approaches, handling some elements internally while seeking expert support for specialised areas like Scope 3 strategy, audit preparation, or board education. The key is honest assessment of internal capabilities and strategic use of external expertise.

What happens if we don't comply with ASRS?

Non-compliance with ASRS can result in regulatory penalties under the Corporations Act, potential legal action from shareholders or stakeholders, damage to reputation and market position, and difficulties accessing capital from ESG-focused investors.

How does ASRS relate to other sustainability frameworks?

ASRS aligns with international standards including TCFD (Task Force on Climate-related Financial Disclosures) and IFRS Sustainability Standards. Companies with existing TCFD reporting will find many requirements familiar, though ASRS has specific Australian regulatory context and assurance requirements.

A one-page visual of the four AASB S2 pillars, what each requires, key deadlines, and the step-by-step compliance path. Start here if your team is scoping what ASRS S2 actually involves.

Benchmark your readiness against 20+ ASRS compliant Australian companies. Includes buying criteria, support gaps, and how first-round filers are approaching year one.

Templates, checklists and frameworks to start your AASB S2 implementation. Built for finance and sustainability leads who are ready to move.

A 5-minute self-assessment. Get a compliance gap map and personalised next steps, scored against the four AASB S2 pillars.

London - Sydney

.png)

.webp)

.png)