Which part of ASRS compliance keeps Australian CFOs awake at night?

If you picked Scope 3, you're in good company.

Nearly every Australian business preparing for ASRS compliance shares the same insight: Scope 3 emissions is a barrier. Companies feel confident measuring direct operations and purchased energy, but moving into value-chain impacts and things get more difficult.

"Scope 1 and 2 are relatively easy for us - Scope 3 is where it gets really messy," confided one engineering firm CFO, a sentiment echoing across industries from retail to professional services.

Scope 3 emissions typically represent 70-90% of most companies' total carbon footprint.

But there's actually good news:

Download The ASRS Pulse Report

Scope 3 emissions encompass all indirect greenhouse gas emissions that occur in your value chain - both upstream and downstream from your direct operations. While Scope 1 covers emissions you directly control and Scope 2 covers the emissions from energy you purchase, Scope 3 includes everything else that happens because of your business activities.

The Greenhouse Gas Protocol defines 15 categories of Scope 3 emissions, split between upstream and downstream activities:

Upstream Categories (Supplier-Related):

Downstream Categories (Customer-Related): 9. Downstream transportation and distribution 10. Processing of sold products 11. Use of sold products 12. End-of-life treatment of sold products 13. Downstream leased assets 14. Franchises 15. Investments

Control and Influence Unlike Scope 1 and 2 emissions, which occur within your direct operational control, Scope 3 emissions happen across your entire value chain. You don't own the suppliers, customers, or transportation companies, but your business decisions influence their emissions.

Data Availability Your electricity meter provides precise Scope 2 data. Your fuel purchases give exact Scope 1 figures. But getting emissions data from hundreds of suppliers or understanding how customers use your products? That's an entirely different challenge.

Methodological Complexity Scope 3 calculations often rely on estimates, spend-based data, and industry averages rather than precise measurements. This introduces uncertainty and makes setting credible reduction targets much more difficult. It also adds complexity when considering assurance.

Our research with over 20 companies preparing for ASRS revealed consistent struggles with Scope 3 implementation. Here's what they're actually experiencing:

"We have over 400 suppliers, and maybe 10% of them have any emissions data they can share," reported a sustainability manager at a manufacturing company. This data gap is universal across industries.

The Supplier Response Problem Companies describe a familiar pattern: they send requests for emissions data to suppliers and receive:

Resource Intensity Getting even basic responses requires significant supplier relationship management. Companies report dedicating full-time staff to supplier engagement just for emissions data collection.

Small Supplier Challenges While large suppliers increasingly have sustainability teams, small and medium suppliers often lack the resources to calculate their own emissions, creating a bottleneck in the supply chain.

"We're constantly worried about double counting, but we're not even sure what we're counting once," admitted a CFO preparing for ASRS compliance. This uncertainty stems from several sources:

Emission Factor Variations Different databases provide different emission factors for the same activities, leading to significant variations in calculated emissions. Companies struggle to know which factors to use and how to document their choices.

Boundary Definition Where does your responsibility end and your supplier's begin? For example, if you pay for shipping, is that your Scope 3 or your supplier's Scope 1? These boundary questions create both methodological complexity and potential double counting.

Activity vs. Spend-Based Approaches Activity-based calculations (using actual quantities) are more accurate but require detailed data that's often unavailable. Spend-based calculations (using financial data and emission factors) are more feasible but less precise.

Even companies that successfully measure Scope 3 emissions struggle with the next step: setting reduction targets that are both ambitious and achievable.

"We can handle our emissions… but we need help bridging the gap to metrics and targets," explained one sustainability lead, capturing a universal challenge.

The Influence vs. Control Problem How do you commit to reducing emissions you don't directly control? Companies struggle to balance ambitious targets with realistic assessments of their influence over suppliers and customers.

Timeframe Misalignment Your suppliers may be on different sustainability timelines than your company. Committing to science-based targets when your supply chain isn't aligned creates implementation challenges.

Verification and Assurance Setting targets is one thing; proving progress against those targets for audit purposes is another. Companies worry about the assurance implications of Scope 3 target commitments.

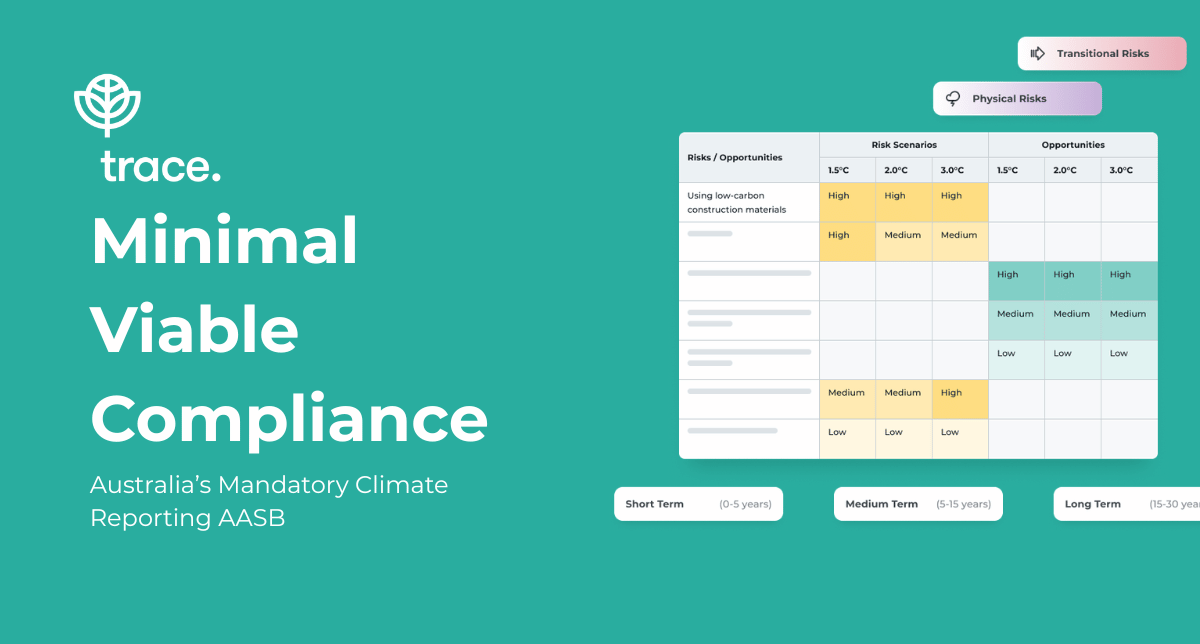

Understanding what ASRS actually requires for Scope 3 reporting helps focus your efforts on compliance-critical elements rather than getting lost in methodological perfectionism.

Scope 3 Emissions Measurement ASRS requires disclosure of Scope 3 emissions "when they are material and it is practical to obtain the information." This materiality threshold provides some flexibility, but most companies find that Scope 3 emissions are clearly material given their size.

Category-Level Reporting You must disclose Scope 3 emissions by category (the 15 categories mentioned earlier), not just as a total figure. This requires understanding which categories are most relevant to your business.

Methodological Disclosure ASRS requires explanation of the methods used to calculate Scope 3 emissions, including:

Crucially, ASRS provides a one-year relief period for Scope 3 emissions reporting. This means:

This relief period is designed to give companies time to:

ASRS allows for limited assurance on Scope 3 emissions in early years, recognizing the inherent uncertainty in value-chain data. However, auditors will still expect:

.png)

Trace works with businesses at every stage of their mandatory reporting journey, from first emissions measurement to audit-ready ASRS S2 disclosure. Talk to our team to see how we can help.

Based on the experiences of companies already tackling Scope 3, here are proven approaches to managing value-chain emissions reporting:

Before diving into data collection, spend time understanding which Scope 3 categories are most material for your business:

Screening Exercise Use spend-based calculations to get rough estimates across all 15 categories. This helps identify which categories represent the largest emissions (often purchased goods and services for most companies).

Supplier Concentration Analysis Identify which suppliers represent the largest portion of your emissions. Often, the top 20% of suppliers by spend account for 80% of supply chain emissions.

Strategic Relevance Consider which categories align with your business strategy and where you have the most influence. Focus initial efforts on areas where you can drive meaningful change.

Successful Scope 3 programs treat supplier engagement as a multi-year relationship-building exercise, not a one-time data request:

Tiered Approach

Supplier Support Programs Leading companies provide resources to help suppliers calculate their emissions:

Contractual Integration Include sustainability reporting requirements in new supplier contracts and renewal discussions. Make climate data sharing a standard part of the commercial relationship.

Establish systems to collect, validate, and manage Scope 3 data consistently:

Data Validation Protocols

Estimation Methodologies Develop consistent approaches for data gaps:

Technology Solutions Consider carbon accounting software that can:

Once you have baseline data, develop realistic but ambitious Scope 3 targets:

Science-Based Target Alignment Align Scope 3 targets with climate science requirements (typically 2.5% annual reduction for most sectors) while considering your actual influence over the value chain.

Supplier Engagement Metrics Set intermediate targets for supplier engagement:

Collaborative Approaches Consider industry collaborations or sector initiatives that can amplify your influence:

Given the one-year ASRS relief period, here's a practical timeline for Scope 3 implementation:

Executive Sponsorship Scope 3 programs require significant supplier relationship management and cross-functional coordination. Executive sponsorship helps open doors and prioritise resources.

Cross-Functional Integration Successful programs integrate sustainability teams with procurement, operations, and supplier management functions rather than treating it as a standalone project.

Long-Term Perspective Scope 3 programs are multi-year initiatives that improve over time. Don't expect perfect data in year one, so focus on building systems and relationships that will deliver better results over time.

If you're just beginning your Scope 3 journey, here's where to focus your immediate efforts:

Remember: The goal in your first year isn't perfection. Instead it's building the foundation for continuous improvement. Focus on establishing processes, relationships, and systems that will deliver better data and outcomes over time.

Scope 3 emissions represent the most complex aspect of ASRS compliance, but they're also where the greatest opportunities lie for genuine supply chain transformation and competitive differentiation.

The companies succeeding in this space share several common approaches:

The one-year ASRS relief period provides valuable time to build these capabilities thoughtfully. Use this time to:

Most importantly, remember that Scope 3 success is measured not just in data accuracy, but in the strength of relationships and systems you build along the way. The companies treating this as a long-term capability-building exercise rather than a compliance checkbox are the ones positioning themselves for genuine competitive advantage in a carbon-constrained economy.

Your Scope 3 journey starts with a single step: understanding what matters most for your business and beginning the conversation with your most important suppliers. The rest will follow from there.

What are Scope 3 emissions and why are they important for ASRS?

Scope 3 emissions are all indirect greenhouse gas emissions in your value chain - from suppliers to customers to waste disposal. They typically represent 70-90% of most companies' total carbon footprint and are required under ASRS from the second reporting year, making them critical for comprehensive climate disclosure.

When do I need to start reporting Scope 3 emissions under ASRS?

ASRS provides a one-year relief period for Scope 3 reporting. While Scope 1 and 2 emissions are required from the first reporting year (FY2025), Scope 3 emissions become mandatory from the second year (FY2026). However, starting preparation immediately is recommended given the complexity involved.

How do I collect Scope 3 data from suppliers who don't track emissions?

Start with a tiered approach: request detailed data from your largest suppliers while using spend-based estimates for smaller ones. If you need to, you can use spend based calculations across all suppliers. Provide support tools and resources to help suppliers calculate their emissions. Consider industry collaborations and supplier development programs to build capability across your supply chain.

What if my suppliers won't provide emissions data?

Begin with education and support rather than demands. Explain the business case for emissions reporting and offer tools to help suppliers get started. Consider making sustainability reporting a factor in future supplier selection and contract renewals. Use industry-average emission factors for non-responsive suppliers while documenting your engagement efforts.

Can I estimate Scope 3 emissions instead of measuring them precisely?

Yes, ASRS allows for estimates when precise measurement isn't practical, especially in early years. The key is documenting your estimation methods, being transparent about limitations, and showing continuous improvement in data quality over time. Spend-based calculations using emission factors are commonly accepted estimation approaches.

How do I set realistic Scope 3 reduction targets?

Focus on areas where you have the most influence and can drive meaningful change. Set both outcome targets (emission reductions) and process targets (supplier engagement metrics). Consider science-based target methodologies but adapt them to your actual influence over the value chain. Start with achievable targets that can be strengthened as your capabilities mature.

What will auditors look for in Scope 3 reporting?

Auditors expect documented methodologies, evidence of data collection efforts, clear explanations of limitations and assumptions, and consistent application of chosen approaches. They understand that Scope 3 data involves estimates and uncertainties - the key is transparency and systematic approaches rather than perfection.

A one-page visual of the four AASB S2 pillars, what each requires, key deadlines, and the step-by-step compliance path. Start here if your team is scoping what ASRS S2 actually involves.

Benchmark your readiness against 20+ ASRS compliant Australian companies. Includes buying criteria, support gaps, and how first-round filers are approaching year one.

Templates, checklists and frameworks to start your AASB S2 implementation. Built for finance and sustainability leads who are ready to move.

A 5-minute self-assessment. Get a compliance gap map and personalised next steps, scored against the four AASB S2 pillars.

London - Sydney

.png)

.webp)

.png)