.png)

The Australian Accounting Standards Board (AASB) has published Exposure Draft ED SR1 Australian Reporting Standards - Disclosure of Climate-related Financial Information which is a long-winded way of announcing that climate-related disclosure just got one step closer to being legislated in Australia. This Exposure Draft is a document that clearly proposes the format for climate-related financial disclosure standards, as well as actively seeks feedback from Australian entities with clear and guided questions.

ED SR1 has been developed using the International Sustainability Standards Board’s (ISSB) two inaugural standards - IFRS S1 and IFRS S2 - as a baseline. It includes three draft Australian Sustainability Reporting Standards (ASRS Standards):

The AASB is a Commonwealth entity under ASIC that develops Australian Sustainability Reporting Standards. The publication of an Exposure Draft is part of the due process that the AASB follows to develop new Australian Sustainability Reporting Standards. Exposure drafts are designed to seek public comment on the AASB’s proposal.

The preparation of financial statements are required under Australian Accounting Standards to consider climate-related matters when the effects of those climate-related matters are material to users of the financial statements. It is now clear the climate risk - both physical and transitional - are material to all entities in Australia. Further, there is a global precedent set by leading economies like the UK and EU for corporations to lead the way on reporting their climate-related risks and opportunities.

There has been accelerated demand for the AASB to expand the scope of its work and develop explicit guidance on climate-related disclosure, especially in light of the global standards produced by the ISSB. The ISSB released its watershed standards, IFRS S1 and S2, earlier in 2023 to set a common language and shared baseline for climate reporting by private entities. This Exposure Draft uses IFRS S1 and IFRS S2 as the baseline.

The Australian Government has announced its commitment to introducing internationally-aligned mandatory climate-related financial reporting for large businesses and financial institutions. As part of this commitment, the Government decided:

(a) the Australian Government Department of the Treasury (Treasury) will lead the development of a broad sustainable finance framework for large businesses and financial institutions, of which climate-related financial disclosure will form one part,3 and the Department of Finance will lead the related work to implement appropriate arrangements for comparable Commonwealth public sector entities to disclose their exposure to climate-related risks and opportunities;

(b) to introduce standardised reporting requirements for large businesses and financial institutions to make disclosures regarding governance, strategy, risk management, and metrics and targets—the four pillars in the TCFD Recommendations, which have been applied by some Australian entities since 2017;

(c) to align as far as possible with IFRS S2 Climate-related Disclosures issued by the ISSB; 4 and;

(d) to amend the Australian Securities and Investments Commission Act 2001 to empower the AASB to deliver Australian Sustainability Reporting Standards to meet the Australian Government’s commitment.

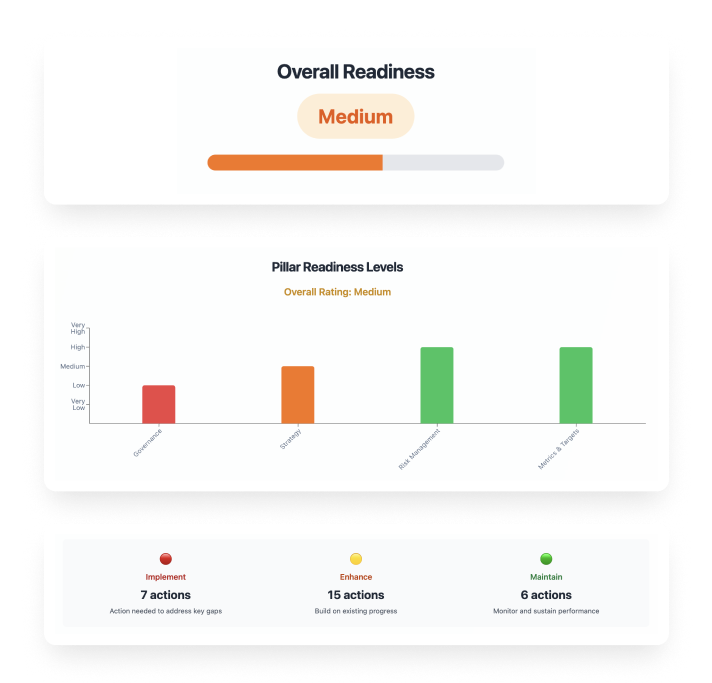

It's a great question. Businesses large and small that are not caught by the legislation, will be caught by implication. To be specific, if your company is not captured under the three legislative phases of climate reporting proposed, your company will almost definitely be caught by the implications of failing to act. The subtext of targetting big businesses in the ASX300 is that small businesses make up all of these big businesses' Scope 3 emissions. This means that thousands of SMEs are about to be asked by their biggest client for a carbon report - we've already seen two of these requests first-hand.

Here are some key questions to consider:

- Are climate issues material to your business? Think physical, supply change, reputation and transitional risks.

- Are your climate change strategies ready for disclosure? Think carbon footprint report by scope and decarbonisation plan with emissions targets.

- Do you have a governance structure providing oversight of sustainability issues? Think sustainable procurement policies, sustainable travel policies etc.

- Where are the gaps between current and future-state reporting? Do you have your carbon accounting provider set up with your data?

- Does your organisation have access to the right knowledge/skills to address those reporting gaps?

- Do you have the right systems and processes in place to collect data?

London - Sydney

.png)

.png)

.png)