Most Australian businesses preparing for ASRS share one thing: they know they need to act, but they don't know where to begin. The standard is complex, the timelines are tight, and the consulting industry hasn't made it easier, with scoping proposals and six-figure quotes arriving before anyone has a clear picture of what's actually required.

This guide cuts through that. It won't explain every clause of AASB S2. It will tell you what to do first, in order, so you can move from overwhelmed to in control.

Nine steps sounds like a lot. In practice, several run concurrently. Think of it as a project plan, not a queue.

ASRS compliance is not a sustainability project. It is a regulated financial disclosure obligation, similar to financial reporting but focused on climate risk and emissions. That framing matters, because it shapes who should own it, how it gets resourced, and what "good" looks like.

Good in year one is defensible, auditable, and complete. Not comprehensive, not sophisticated, not award-winning. Proportionate and audit-ready is the standard. Keep that in mind as you work through the steps below.

The short answer: ASRS applies to Australian entities meeting size thresholds under the Corporations Act. Reporting is phased across three groups, with different start dates and obligations for each.

The first step is simple: find out which group you fall into.

Group 1 (reporting periods starting on or after 1 January 2025): Listed entities or unlisted public companies meeting at least two of: 500+ employees, $1 billion+ in consolidated gross assets, or $500 million+ in consolidated revenue.

Group 2 (reporting periods starting on or after 1 July 2026): Entities meeting at least two of: 250+ employees, $500 million+ in consolidated gross assets, or $200 million+ in consolidated revenue.

Group 3 (reporting periods starting on or after 1 July 2027): All other entities required to lodge financial reports with ASIC that meet the lower legislated size thresholds.

If you are a Group 1 or Group 2 entity reading this in 2025 or 2026 and haven't started, you are already working in a compressed timeline. If you're Group 3, you have more runway, but the preparation requirements are the same.

Check your status with your external auditor or on the ASIC website. Don't assume you're out of scope.

This step sounds obvious, but it is where most organisations stall. ASRS compliance sits uncomfortably across finance, legal, sustainability, and operations. Nobody owns it clearly, so nobody moves.

Appoint one person with genuine authority to coordinate across teams and escalate to leadership. In most Group 2 and 3 organisations, this is a senior finance or risk role, not a sustainability specialist. The lead doesn't need to understand climate science. They need to know how to run a cross-functional project with a hard regulatory deadline.

Give this person a budget, a timeline, and direct access to the CFO or CEO. Without that authority, the project will stall at the first data collection request.

One practical note: Treasury estimates ASRS preparation will cost large organisations $750,000 to $1.6 million using traditional advisory models. That figure drops significantly when the right tools and a structured approach are used from the start. Appointing a capable internal lead is one of the most effective ways to control that cost.

Before you build anything, understand what you're starting with. A gap assessment answers four questions:

Work through each of the four ASRS disclosure pillars (governance, strategy, risk management, and metrics and targets) and document what exists and what doesn't. The gaps become your project plan.

Most organisations find that governance documentation and climate risk assessment require the most new work. Emissions data collection is usually the most time-consuming. Disclosure drafting comes last, once the underlying substance is in place.

Many specialist climate reporting providers offer structured readiness assessments as a starting point. These are a facilitated review of where your organisation stands across all four ASRS pillars, with a clear output on gaps, priorities, and a realistic view of timeline and cost. If you want to move quickly without doing the desktop work yourself, a structured readiness assessment is the most efficient first step. Trace offers a free ASRS readiness quiz that gives you an instant view of where your organisation stands across the four disclosure pillars.

See also: what an ASRS readiness assessment covers and how to use one

.png)

Trace works with businesses at every stage of their mandatory reporting journey, from first emissions measurement to audit-ready ASRS S2 disclosure. Talk to our team to see how we can help.

ASRS requires directors to attest to the accuracy of climate disclosures, in the same way they sign off on financial statements. That is a material accountability, and most boards are not yet prepared for it.

You don't need a full board training programme. You do need to:

A single well-structured board presentation, followed by documented minutes, satisfies a significant portion of the governance disclosure requirement. What matters is documentation: what was discussed, when, and what decisions or actions followed.

This step belongs here, before you start measuring anything. The platform and expert support you put in place will determine how your emissions data is collected, structured, and evidenced. Making these decisions after the fact creates rework and audit risk.

There is a wide range of options available, from full-service consulting engagements to self-serve software platforms. The right combination depends on your internal capacity, your timeline, and the complexity of your business structure.

A few things worth looking for:

Australian regulatory alignment. The platform should be built around AASB S2 and ASRS, not adapted from a global framework. Calculation methodology needs to reflect Australian emissions factors, Australian grid data, and Australian assurance expectations.

Audit trail generation. Whatever you use must produce an evidence record that external auditors can review without your assistance. Assembling this manually after the fact creates unnecessary risk and effort.

Access to expert guidance. Software alone is not enough for most first-time reporters. You need access to specialists who can confirm your emissions boundary, validate your climate risk approach, and support you during assurance. Check whether that is included or charged separately at hourly rates.

Transparent pricing. Watch for models that bundle advisory time into platform fees in opaque ways. The lowest upfront cost is rarely the most cost-effective across three to five annual reporting cycles.

For a full comparison of platforms available to Australian businesses, see ASRS software and tools: the Australian business guide (2026 comparison.

This is where most of the project effort sits. Emissions measurement underpins your metrics and targets disclosure, but it also feeds your strategy and risk disclosures, so it needs to be in place before the report can be drafted.

In year one, the minimum requirement is Scope 1 and 2 emissions. Scope 3 is required progressively, with Group 1 entities expected to address material categories from the start and Group 2 and 3 building coverage over time. If you're a first-time reporter, get Scope 1 and 2 right before expanding further.

For Scope 1 and 2, you need:

Manual spreadsheets are possible in year one, but they carry real risk. A single formula error or inconsistent methodology becomes an audit finding. Purpose-built carbon accounting software automates the calculation, enforces methodology consistency, and generates the audit trail automatically, which is why the tool and support decisions in Step 5 matter before this work begins.

For Scope 3, start with a category screen before you measure anything. The GHG Protocol defines 15 Scope 3 categories. Most organisations have two or three that are material to their business. Screen first, measure second. Don't attempt to cover everything at once.

See also: latest Scope 3 guidance from the GHG protocol

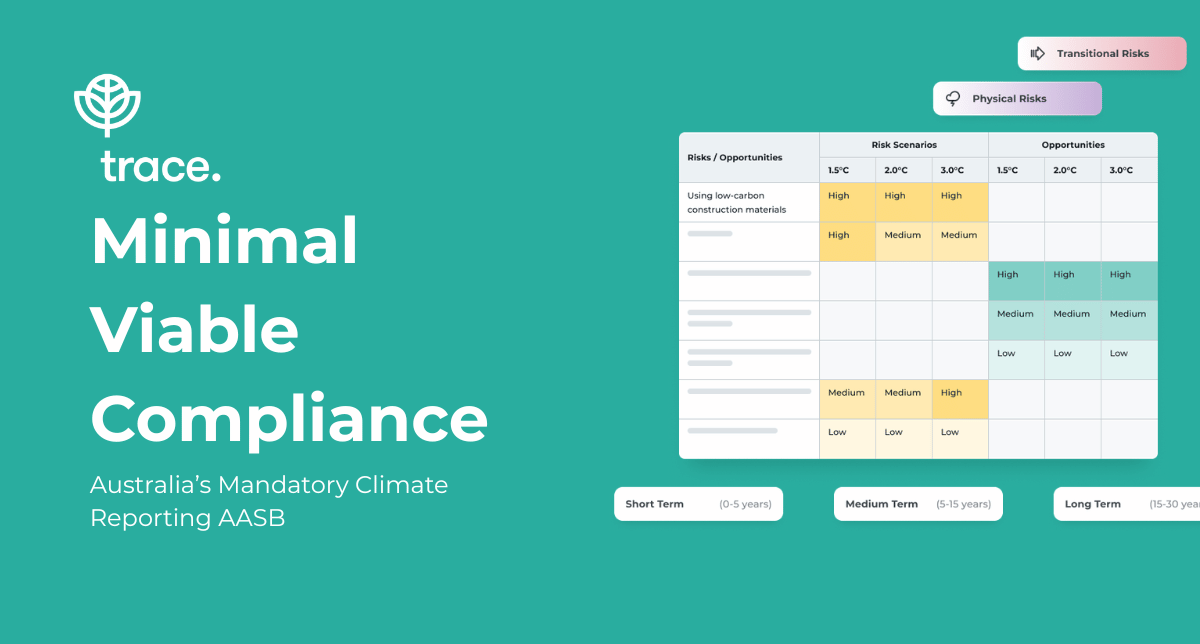

Climate risk assessment is not optional commentary. It is a core ASRS requirement sitting under the Strategy and Risk Management pillars, and it needs to be in place before your disclosure can be drafted.

AASB S2 requires you to assess how your business performs under at least two climate scenarios: one consistent with limiting warming to around 1.5 degrees Celsius (a rapid transition to a low-carbon economy), and one reflecting higher physical risk (where warming tracks toward 3 degrees or above). The purpose is to test whether your current strategy is resilient to plausible climate futures, and to disclose where it is and isn't.

In year one, qualitative disclosure is acceptable for most entities. You are not required to produce financial modelling or asset-level quantitative analysis from day one. What is required is a structured, documented process, not a desk-based guess.

A defensible year-one climate risk assessment includes:

One practical point: the climate risk assessment and the emissions measurement work can run in parallel. You don't need to finish one before starting the other. But both need to be complete before the disclosure can be drafted, because they feed different sections of the report.

For most Group 2 and 3 entities, a structured, expert-led assessment takes four to eight weeks. If your timeline is compressed, this is one of the workstreams where specialist support has the greatest impact on both quality and speed.

The most common mistake in first-year ASRS disclosures is overbuilding. Organisations spend too long trying to make every section comprehensive and polished, when what auditors actually look for is completeness, consistency, and a traceable audit trail.

Your year-one disclosure should:

Year one is a baseline. Year two is where you refine data coverage, strengthen your Scope 3, and deepen your risk analysis. The organisations that handle ASRS well treat it like financial reporting: structured, owned internally, annual, and incremental.

As one Group 1 CFO put it during Trace's recent ASRS breakfast briefings: first-round disclosures from comparable entities are running 30 to 40 pages. Some of the better-positioned organisations are targeting eight. Concise and defensible outperforms lengthy and unstructured every time.

Assurance is not something that happens to your disclosure after it's finished. It is a process that needs to be built into the work from the start, and engaging your assurance provider early is one of the most important things a first-time reporter can do.

AASB S2 requires limited assurance over climate disclosures in year one, moving to reasonable assurance by year four. Limited assurance is less intensive than the reasonable assurance applied to financial statements, but it still requires your assurance provider to review your emissions data, methodology, and underlying evidence, and form a conclusion on whether your disclosures are materially correct.

What that means in practice:

Engage early, not at the end. Your external auditor or appointed assurance provider should know what you're doing before you submit a draft disclosure. Engaging them after the fact, with a finished document and no audit trail, is where costs blow out and findings emerge.

Understand their evidence requirements. Different assurance providers set different evidence thresholds. Ask early: what do you need to see for each assertion in the disclosure? What does the emissions audit trail need to include? What level of documentation is required for the climate risk assessment? The answers should shape how you build the work, not how you retrospectively document it.

Build the audit trail as you go. The most common source of assurance findings is not incorrect data. It is missing or incomplete documentation: an emission factor that can't be traced to a source, a methodology decision that was made verbally and never written down, a boundary assumption that isn't formally recorded. Document every decision at the time it's made.

Budget for it. Assurance costs for a first-time ASRS reporter typically range from $15,000 to $50,000 depending on the size and complexity of the organisation, the scope of emissions covered, and the assurance provider. This is a separate cost from advisory or platform fees and should be in your year-one budget.

For most Group 2 and 3 organisations, establishing the foundations for year-one compliance, including governance documentation, a defensible Scope 1 and 2 baseline, and a structured climate risk assessment, takes three to six months of concentrated effort. Disclosure drafting adds another six to eight weeks.

If your Group 2 reporting period starts 1 July 2026 and you haven't begun, that window is narrow. The risk of delay isn't just a worse disclosure. It's a more expensive and more disruptive one, with less time to surface issues before they become audit findings.

If you want a structured view of where your organisation stands before committing to a plan, start with Trace's free ASRS readiness quiz. It takes two minutes and gives you an instant read on where your organisation stands across each of the four ASRS disclosure pillars.

If you'd prefer to talk through your situation directly, book a 30-minute call with the Trace team to get a clear picture of what's ahead and what a realistic programme looks like for your organisation.

Trace is a climate reporting platform specialising in ISSB and AASB standards, helping businesses navigate mandatory climate disclosure with clarity and confidence.

A one-page visual of the four AASB S2 pillars, what each requires, key deadlines, and the step-by-step compliance path. Start here if your team is scoping what ASRS S2 actually involves.

Benchmark your readiness against 20+ ASRS compliant Australian companies. Includes buying criteria, support gaps, and how first-round filers are approaching year one.

Templates, checklists and frameworks to start your AASB S2 implementation. Built for finance and sustainability leads who are ready to move.

A 5-minute self-assessment. Get a compliance gap map and personalised next steps, scored against the four AASB S2 pillars.

London - Sydney

.png)

.webp)

.png)